Managing finances can be challenging for anyone, but it becomes particularly crucial when you’re part of a single-income household. Whether you’re supporting a family on one salary or living alone with one income, having a solid budget can make all the difference.

In this article, we will provide you with essential budgeting tips tailored specifically for single-income households. These strategies will help you make the most of your income, avoid debt, and build a secure financial future.

In today’s economic climate, managing finances on a single income requires careful planning and disciplined spending.

Single-income households face unique challenges, including the risk of financial instability if the sole income source is disrupted. However, with effective budgeting, you can ensure that your financial situation remains stable and secure.

This guide provides valuable budgeting tips designed specifically for single-income households, helping you make the most of your earnings and achieve your financial goals.

Budgeting Tips for Single-Income Households

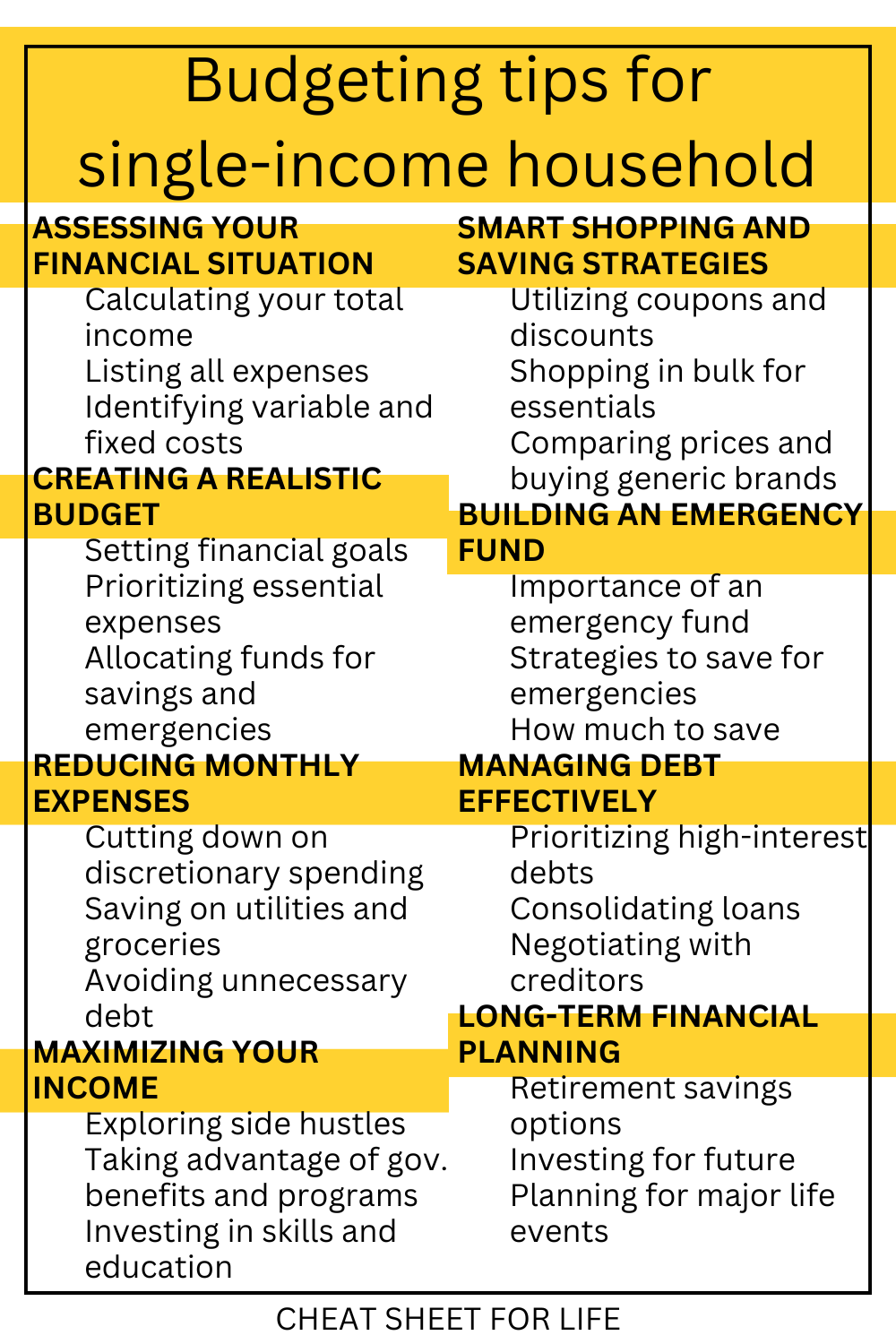

Assessing Your Financial Situation

The first step in effective budgeting is understanding your financial situation. Begin by calculating your total monthly income. This includes your salary, any additional income sources, and government benefits. Next, list all your expenses. Categorize them into fixed costs (rent, utilities, insurance) and variable costs (groceries, entertainment, transportation). This detailed overview will help you identify where your money is going and where you can make adjustments.

Creating a Realistic Budget

Once you have a clear picture of your finances, it’s time to create a budget. Start by setting short-term and long-term financial goals. Prioritize essential expenses such as housing, utilities, and food. Allocate a portion of your income to savings and emergency funds. It’s crucial to be realistic and flexible with your budget to accommodate unexpected expenses and changes in income.

Budgeting notebooks truly come in handy here because you can make plans, track your spending, and always stay on top of your finances, all in one place. If you don’t want to create your own budgeting notebook, check out this overview of 15 affordable budgeting notebooks and what they have to offer.

Reducing Monthly Expenses

One of the most effective ways to manage a single-income household is to reduce monthly expenses. Begin by cutting down on discretionary spending like dining out, subscriptions, and entertainment. Look for ways to save on utilities, such as using energy-efficient appliances and reducing water usage. When it comes to groceries, plan your meals, make a shopping list, and stick to it to avoid impulse buys. Additionally, avoid accumulating unnecessary debt by using credit cards wisely and paying off balances in full each month.

Learn how to save on grocery bills while still eating healthily.

Maximizing Your Income

To supplement your primary income, consider exploring side hustles or freelance work that aligns with your skills and interests. This extra income can help you achieve financial stability faster. Additionally, take advantage of government benefits and programs designed to support single-income households. Investing in your education and skills can also open up opportunities for better-paying jobs and career advancement.

To increase your income you can try your hand at one of many home-based side hustles.

You could also explore different ways of making money through Amazon even if you don’t have a product to sell.

Smart Shopping and Saving Strategies

Being a savvy shopper can significantly impact your budget. Use coupons and take advantage of discounts whenever possible. Buying in bulk can save money on essentials like toiletries and non-perishable foods. Compare prices and consider purchasing generic brands, which are often just as good as name-brand products. Planning and sticking to a shopping list can prevent overspending and impulse purchases.

If you’re a frequent Amazon shopper keep this list of monthly sales at hand, and know all the places where you can find coupons and promo codes.

Building an Emergency Fund

An emergency fund is essential for single-income households. It provides a financial cushion in case of unexpected events such as job loss, medical emergencies, or major repairs. Aim to save at least three to six months’ worth of living expenses. Start small if necessary, but consistently contribute to your emergency fund until you reach your goal.

Managing Debt Effectively

If you have existing debt, managing it effectively is crucial. Focus on paying off high-interest debts first, as they can quickly accumulate and become unmanageable. Consider consolidating loans to reduce interest rates and simplify payments. If you’re struggling to make payments, reach out to creditors to negotiate more favorable terms or payment plans.

Long-Term Financial Planning

Planning for the future is just as important as managing current expenses. Explore retirement savings options. Investing in stocks, bonds, or mutual funds can help grow your wealth over time. Additionally, plan for major life events such as buying a home, starting a family, or funding education. Long-term planning ensures you’re prepared for life’s milestones and can achieve your financial aspirations.

Try creating your financial freedom vision board to keep you focused on your long-term goals. Eyes on the prize is not just an empty saying, holding your financial goals in your mind will positively affect your behavior and encourage you to make choices that will support your goal.

Living on a single income presents challenges, but with careful budgeting and strategic planning, you can achieve financial stability and peace of mind. By assessing your financial situation, creating a realistic budget, reducing expenses, maximizing income, and planning for the future, you can make the most of your resources.

Stay disciplined, be adaptable, and remember that every small step you take today brings you closer to a secure financial future.